An Overview of Peptide Therapeutics and its Contract Manufacturing Market

The introduction of insulin therapy in the 1920s, for the treatment of diabetes, marked the beginning of the therapeutic use of peptides. Presently, peptide-based therapeutics represent a prominent class of therapeutic interventions. Currently, many peptide therapeutics are being developed for the treatment of oncological disorders. In fact, in 2018, about 75% of such therapeutic products were estimated to be available for the treatment of different cancer indications, accounting for global sales of more than USD 1 billion. It is worth highlighting that, till date, more than 60 peptide drugs have been approved by the United States Food and Drug Association (USFDA), while more than 400 peptides are presently being in clinical trials.

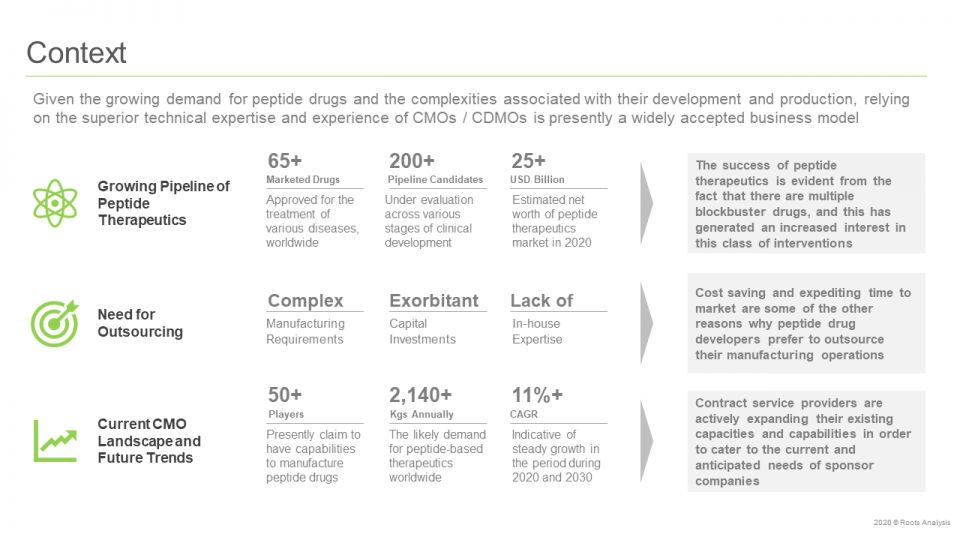

Such therapeutics, when compared to recombinant antibodies and protein-based interventions, have been shown to demonstrate better tissue / cell penetration, owing to their small size and low immunogenicity. Further, the need for advanced technologies, along with specialized equipment, have resulted in the outsourcing of the peptide production to the contract manufacturers. The contract manufacturing market in this domain features the presence of large contract manufacturing organizations (CMO), mid-sized CMO and small companies.

A contract manufacturer is a third-party organization that offers manufacturing related services on a contract basis to other firms. Typically, a client may approach a contract manufacturing firm after conducting initial R&D for a product and employ its services to manufacture the product, usually at larger scales.

The “Peptide Therapeutics: Contract API Manufacturing Market, 2020-2030” report features an extensive study of the current market landscape and future opportunities associated with the contract manufacturing of therapeutic peptides. The study also features a detailed analysis of key drivers and trends related to this evolving domain. Amongst other elements, the report includes:

- A detailed review of the overall landscape of companies offering contract services for manufacturing of peptides, along with information on year of establishment, company size, scale of operation (preclinical, clinical and commercial), geographical location of CMO, number and location of their respective facilities, type of peptide synthesis method used, type of peptide modification services offered, peptide purification technology used, and regulatory accreditations / certifications.

- An analysis on the recent developments in the industry, highlighting collaborations, facility expansions, and upcoming peptide synthesis technologies within this domain.

- Informed estimates of the annual commercial and clinical demand for manufacturing peptides for therapeutic use, based on various relevant parameters, such as target patient population, dosing frequency and dose strength.

- A clinical trial analysis of completed, and active studies related to peptide therapeutics that are have been / being / likely to be conducted across various geographies, based on the trial registration year, trial phase, trial recruitment status, therapeutic areas type of sponsor / collaborator, geography and number of patients enrolled.

- An estimate of the overall, installed capacity for manufacturing peptides, based on data reported by industry stakeholders in the public domain; it highlights the distribution of available peptide production capacity across companies of different sizes (small, mid-sized, large and very large firms), scale of operation (clinical and commercial), and key geographical regions (North America, Europe, Asia Pacific).

- A discussion on regulatory guidelines related to peptide manufacturing, highlighting key differences across various geographies, including the US, Europe, Australia, China, India, Japan and South Korea. It also includes details related to the various challenges, related to regulatory scrutiny, faced by peptide manufacturers.

- Elaborate profiles of the key players that offer contract manufacturing services across different geographies, namely North America, Europe and Asia Pacific. Each profile features a brief overview of the company, information on its service portfolio, details related to its manufacturing capabilities and facilities, and an informed future outlook.

- A discussion on industry affiliated trends, key drivers and challenges, under a SWOT framework, which are likely to impact the evolution of this field; it includes a Harvey ball analysis, highlighting the relative impact of each SWOT parameter on industry dynamics.

The in-house development of peptide API requires necessary expertise and capabilities, including design, construction and maintenance of a facility which demands significant capital investments. Therefore, several small drug developers and, at times, certain pharma giants as well, have begun outsourcing their manufacturing operations to contract service providers. The increasing demand for companies capable of offering manufacturing and, in certain cases, development services to biopharmaceutical players has resulted in the establishment of several CMOs. Most of these contract service providers have profound experience in niche and emerging areas. The innate expertise and availability of the required capabilities and infrastructure enables CMOs to effectively fulfil the requirements of their clients, eliminate costly oversights and, thereby, reduce chances of failure.

21053

21053